India's Consumption Boom vs Middle East's Feedstock Advantage: The Future of Polyurethane Markets

- ial

- 3 days ago

- 5 min read

As global polyurethane production shifts towards emerging economies, India and the Middle East have emerged as two of the fastest-growing markets, although their growth is underpinned by some different market dynamics. Both regions are benefiting from the growing domestic demand; although India's growth is largely consumption led, the Middle East combines expanding regional demand with integrated petrochemical production and downstream manufacturing investments.

India’s polyurethane market is projected to grow at a CAGR of 10.0% between 2025 and 2030, driven by rapid urbanisation, a growing manufacturing base, and increasing demand from the construction, automotive, furniture and consumer goods sectors. Government programmes such as Make in India and the Production Linked Incentive (PLI) scheme, alongside rising investment in downstream polyurethane processing, are further strengthening the production capacity.

In contrast, the Middle East market is projected to grow at 5% on average between 2025 and 2030. As well as being driven by domestic consumption, growth in the region is supported by ready supplies of petrochemical feedstocks, integrated production facilities and sustained investment in downstream manufacturing. Government initiatives such as Saudi Arabia's Vision 2030, the UAE's Operation 300bn strategy, and industrial expansion in Oman, together with mega infrastructure projects, expanding tourism and hospitality development across the GCC have further strengthened polyurethane demand.

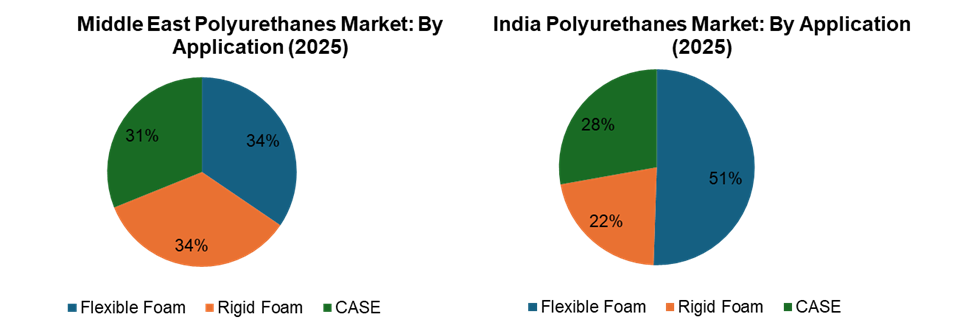

Countries such as Saudi Arabia, Oman and the UAE are consolidating their role as regional production and export centres, while simultaneously diversifying into higher‑value polyurethane applications. Together, these market dynamics position India as one of the fastest‑growing polyurethane markets, while the Middle East continues to leverage its feedstock advantage to strengthen its role within regional and global supply chains. Some divergence is evident in the application mix below.

Source: IAL Consultants

Rigid Foam

Rigid foam continues to be a key application in both India and the Middle East, although demand is driven by different end-use industries. In India, rigid foam accounted for 22% of the polyurethane production in 2025. Continued investment in pharmaceutical cold chain infrastructure, food logistics, refrigerated warehousing and data centres is further supporting demand for rigid foam. In the Middle East, rigid foam accounted for 34% of polyurethane production in 2025, with growth supported by Saudi Arabia’s large‑scale infrastructure projects and Vision 2030 initiatives, alongside the UAE’s expansion of commercial construction. Iran, the UAE and Saudi Arabia are the largest PU rigid foam producers. The fastest growth in 2025 was in Saudi Arabia at 5%.

Major developments including the NEOM project, the Red Sea Project, Diriyah Gate, and expanding district cooling infrastructure across the GCC are expected to maintain long-term demand for rigid polyurethane foam.

Flexible Foam

Flexible foam remains a key application in both India and the Middle East, driven by demand from the furniture, bedding, automotive and footwear industries. In India, slabstock foam accounted for over 60% of total flexible polyurethane output in 2025, with the slabstock production rising by 11%, reflecting demand from the mattress and furniture sectors. Moulded polyurethane foam production also increased, supported by automotive manufacturing and commercial furniture applications. Capacity expansion by organised mattress manufacturers and furniture producers continues to support flexible polyurethane foam demand. In the Middle East, slabstock represented approximately 80% of total flexible foam output in 2025, with conventional polyether foam leading the overall production.

Growth is driven by furniture manufacturing and residential and commercial construction in the UAE and Saudi Arabia, with hospitality projects in Qatar further boosting the demand. Saudi Arabia is by far the largest producer of slabstock in the Middle East, followed by the UAE and Iran. The latter is seeking to build up its domestic polyurethane industry in response to its international isolation and sanctions. Iran is by far the largest producer of moulded foam in the Middle East, reflecting the importance of its automotive industry.

CASE

CASE (Coatings, Adhesives, Sealants and Elastomers) applications continue to gain prominence across India and the Middle East, supported by expanding industrial activity and infrastructure development. India’s CASE market is led by elastomers, reflecting its consumer‑driven industrialisation and automotive expansion, while the Middle East’s coatings growth aligns with infrastructure investment and national diversification strategies.

In India, polyurethane elastomers registered the strongest regional growth at 8% in 2025, supported by rising demand from the automotive and footwear industries, as well as applications in trolley and industrial wheels, gaskets, seals and material‑handling equipment. Although demand for elastomers continues to expand, manufacturers are facing competition from alternative materials such as EPDM and EVA in certain end‑use sectors.

Rising investments in electric vehicle manufacturing and industrial equipment production are also supporting demand for CASE applications.

In the Middle East, polyurethane coatings production rose by 5% in 2025, driven by large-scale infrastructure projects, oil & gas sector requirements, and protective industrial applications. This supports national diversification plans (such as Saudi Vision 2030, the UAE’s industrial strategy). Saudi Arabia and the UAE recorded the strongest growth in 2025, with production increasing by 7% and 5%, respectively.

Raw material Supply

Beyond applications, the two regions differ in terms of raw material availability, supply chains and cost structures. India continues to rely heavily on imported MDI, TDI and polyols, supplied by leading global producers such as Covestro, Wanhua Chemical, BASF, Huntsman and Tosoh. Domestic TDI production is supported by Gujarat Narmada Valley Fertilisers & Chemicals (GNFC), while Manali Petrochemicals leads in polyol manufacturing. Still, imports remain necessary to meet rising demand. Recently, India has imposed anti-dumping duties on selected TDI imports, whilst Manali Petrochemicals is expanding its polyester polyol capacity. At the same time, downstream manufacturers such as Expanded Polymer Systems continue to invest in polyurethane systems production.

On the other hand, the Middle East benefits from abundant oil- and gas-based feedstocks and integrated petrochemical production. Regional competitiveness is reinforced by major petrochemical producers such as SABIC, which supply upstream feedstocks, together with Sadara Chemical Company, one of the largest producers of MDI and TDI. Furthermore, Covestro’s feasibility study for a world-scale MDI facility in the UAE underscores the region’s growing appeal for future isocyanate production and downstream chemical investment.

Despite these advantages, conflict in the Middle East in early 2026 has driven oil prices sharply higher. The war in Iran and the effective closure of the Strait of Hormuz have resulted in the largest supply disruption in the history of the global oil market, according to the International Energy Agency (IEA). Interruptions affecting facilities such as Iran’s Karoon Petrochemical complex (MDI and TDI producer) have highlighted the region’s vulnerability to geopolitical events. While the Middle East retains a certain level of feedstock and cost advantage, India’s import-dependent polyurethane industry remains more susceptible to fluctuations.

Strategic Outlook

Source: IAL Consultants

Although India and the Middle East markets are shaped differently, their strengths are increasingly complementary rather than competitive. India’s increasing domestic demand, together with the Middle East’s feedstock advantage and integrated production capabilities, creates scope for cross‑regional investment, long‑term raw material partnerships and collaboration in downstream manufacturing. As the polyurethane industry continues to evolve, companies that harness these regional synergies will be well-positioned to capitalise on future growth opportunities.

Source: IAL Consultants

For more information, please contact ial@brggroup.com

IAL Consultants (A Division of BRG Enterprise Solutions Ltd)

CP House, 97-107 Uxbridge Road, Ealing, London W5 5TL

Tel: +44 (0) 20 8832 7780