Global Trends in Polyurethane Insulation Additives

- ial

- Feb 24

- 5 min read

Updated: Mar 27

Overview

Polyurethane (PU) foam is among the most versatile insulation materials, prized for thermal performance, strength and adaptability. While polyols and isocyanates form the backbone, additives such as flame retardants and blowing agents can define its safety, efficiency and sustainability.

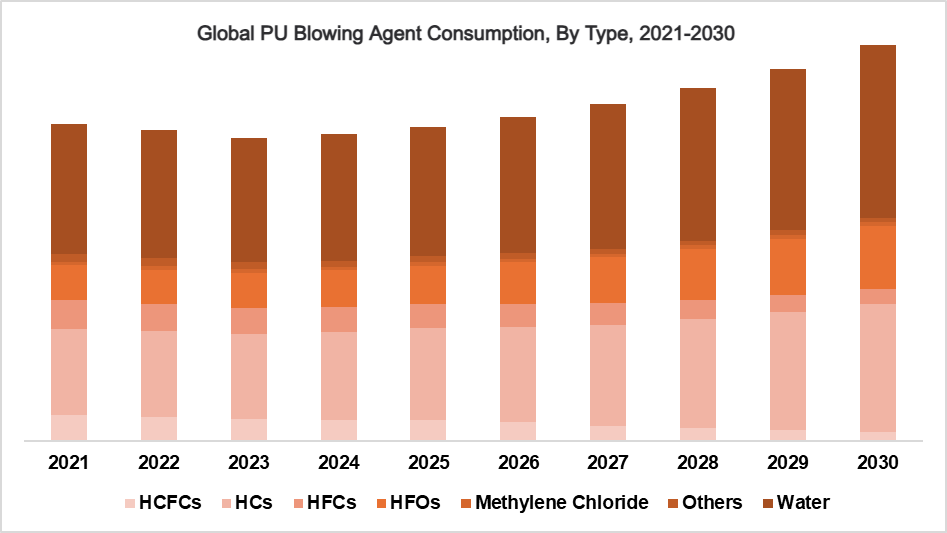

Key PU additives covered in the first edition of IAL’s new study are blowing agents and flame retardants. Blowing agents are critical components in the production of foamed materials used in insulation, packaging and various consumer goods. Their global consumption has been influenced by a mix of regulatory pressures, economic trends and technological advancements. From 2021 to 2024, overall consumption saw a moderate decline. However, starting in 2025, consumption begins a notable upward trajectory. This rebound is driven by industrial recovery, growing construction activity and increased demand for energy efficient insulation materials.

The total additives market for blowing agents and flame retardants was estimated at around ~1.6 million tonnes in 2025 and forecast to reach ~2 million tonnes by 2030, registering a CAGR of 5%. Overall growth is driven by regulatory transitions toward low-GWP blowing agents, increasing construction and insulation demand, and stricter global fire safety standards. Expanding infrastructure investments, urban development and sustainability-driven product innovations across all regions will continue to support steady market expansion through 2030.

The global blowing agent additives market is expected to grow at an overall CAGR of 5% between 2025 and 2030, supported by rising insulation demand, sustainability targets and regulatory-driven technology shifts toward environmentally compliant solutions.

HCFCs are projected to decline significantly at a CAGR of -15%. HCFCs, heavily restricted under the Montreal Protocol, are expected to decline sharply as most countries implement phaseout plans. This reduction is driven by strict regulatory deadlines and replacement by environmentally safer alternatives across both developed and developing markets.

HFCs will also experience a sharp contraction at a CAGR of -9%. HFCs, targeted by the Kigali Amendment due to their high GWP, are facing accelerated phase-down under regulations such as the AIM Act in the US and the EU F-Gas Regulation, pushing the industry toward lower-GWP alternatives.

HFOs are expected to be the fastest-growing segment, expanding at a CAGR of 10%. Low-GWP alternatives are on the rise, with HFOs gaining widespread adoption due to their strong environmental profile and regulatory compliance, making them the preferred replacement for HCFCs and HFCs globally. Hydrocarbons (HCs) are projected to grow at a CAGR of 7%. HCs remain particularly popular in cost-sensitive markets, especially across APAC, although flammability concerns continue to pose safety and regulatory challenges in certain regions.

Water-based blowing agents are expected to grow steadily at a CAGR of 6%. With zero GWP and strong safety advantages, water-based systems are gaining traction, particularly in EMEA and North America, where sustainability targets and safe processing requirements are driving adoption.

In 2025, TCPP remained the most widely used flame retardant globally, accounting for more than 72% of total consumption. However, TCPP is forecast to decline at a CAGR of -2% as the industry gradually shifts away from halogenated compounds due to health and environmental concerns. Countries are increasingly adopting non-halogenated alternatives, particularly across Europe and North America, influenced by REACH restrictions, the US TSCA and growing consumer demand for safer, more sustainable products.

One of the fastest-growing flame retardants is APP, which is projected to expand at a remarkable CAGR of 46% up to 2030. This growth is driven by the rising adoption of APP in halogen-free formulations, especially for insulation panels, cold storage facilities and construction applications. APP is favoured for its excellent thermal stability and environmentally friendly profile, making it well suited to sustainable building practices. The Others segment, representing novel and speciality flame retardants including phosphorus-based and nitrogen compounds, is also expected to grow exponentially, reflecting strong demand for newer, eco-friendly solutions.

Sustainability-Driven Additives: The Next-Gen in Line

Innovation is accelerating, with focus on zero-GWP, bio-based and recyclable additives that align with circular economy goals. At the same time, multifunctional additives are gaining attention for reducing formulation complexity while enhancing both performance and sustainability.

Additives remain the cornerstone of PU insulation’s success, safeguarding against fire risks, enabling thermal efficiency and driving sustainability. Their evolution reflects not just technical progress but strategic responses to global priorities: energy efficiency, climate action and resilient infrastructure. With consumption rising and innovation accelerating, additives will continue to drive the polyurethane industry forward as a cornerstone of energy-efficient and sustainable construction.

Next-generation blowing agents are increasingly centred on low-GWP and sustainable technologies. HFOs are gaining strong traction due to their ultra-low global warming potential and high insulation efficiency in rigid PU foam applications. Several US states are advancing restrictions on PFAS that could constrain the use of HFOs as blowing agents, resulting in varied foam formulations across regions and accelerating the development of non-PFAS alternatives. Industry experts indicate that exemptions for critical HFO applications or phased implementation timelines may be considered to balance climate objectives, given that HFOs offer ultra-low global warming potential compared with the HFCs they replace. As of 2025, the EPA’s TSCA definition excludes HFO and HFC blowing agents used in spray foam from PFAS classification, providing a degree of regulatory clarity. However, fragmented state-level policies continue to create uncertainty for polyurethane applications, including insulation, and no uniform federal ban has yet been finalised.

New innovations, including fifth-generation fluorinated agents with near-zero GWP and no harmful by-products, further support decarbonisation goals while maintaining thermal performance. At the same time, manufacturers such as Dow and Huntsman are expanding water-blown, hydrocarbon (cyclopentane and n-pentane) and methylal-based alternatives, offering cost-effective and environmentally compliant solutions for insulation in construction and appliances. These developments reflect a clear industry shift towards climate-aligned and regulatory-compliant blowing agent technologies.

Sustainability trends are reshaping flame retardant use in PU foams, with traditional halogenated solutions gradually being replaced by halogen-free and bio-based alternatives due to environmental and health concerns. Innovations in phosphorus-based reactive flame retardants, mineral-based additives and advanced coatings are improving fire performance while reducing toxicity and smoke emissions. However, conventional additives such as APP, TEP, expandable graphite, ATH and antimony trioxide remain widely used due to their cost effectiveness and proven performance in meeting fire-safety standards. The market is steadily transitioning towards next-generation options, including organophosphorus compounds and bio-based intumescent systems, reflecting a broader global shift towards safer and more sustainable flame-retardant chemistries.

Research for this study was carried out in late 2025 and early 2026. Data are provided from 2021 to 2030, with the base year 2025. The study reviews the consumption of additives in the polyurethane foam market split by end-use sectors across flexible and rigid foam.

For more information, please contact ial@brggroup.com

IAL Consultants (A Division of BRG Enterprise Solutions Ltd)

CP House, 97-107 Uxbridge Road, Ealing, London W5 5TL

Tel: +44 (0) 20 8832 7780