Global Overview of Flame Retardants in the Polyurethane Foam Market 2026

- ial

- Apr 16

- 4 min read

IAL Consultants is pleased to announce the recent publication of its report on Flame Retardants in the Global Polyurethane Foam Market.

This second edition provides a detailed analysis of the global and regional flame retardant market for polyurethane foams, covering both rigid and flexible foam applications across key industries such as construction, automotive, furniture and appliances. It examines flame retardant chemistries including halogenated, non-halogenated, phosphorus-based, inorganic and emerging sustainable solutions, alongside consumption trends, regulatory developments and technological innovations. The study highlights market trends in flame retardant adoption, showing a clear shift from traditional halogenated products like TCPP to environmentally friendly alternatives such as expandable graphite (EG), ammonium polyphosphate (APP) and aerogels.

Additive flame retardants are generally not used in polyether and polyester flexible polyurethane foams because they compromise the key properties that make these materials valuable, namely low density, softness, elasticity and an open-cell structure. Solid additive flame retardants such as APP, melamine, ATH or expandable graphite require high loadings to be effective, which increases foam density, stiffens the material and reduces resilience and comfort. In addition, these additives can disrupt the foaming process, leading to poor cell formation, foam collapse and uneven rise, making them unsuitable for continuous slabstock or moulded foam production.

All data in this report is based on 2025 as the reference year, with market forecasts through 2030, offering a comprehensive perspective on the evolving landscape of fire safety additives in polyurethane foam markets.

Summary

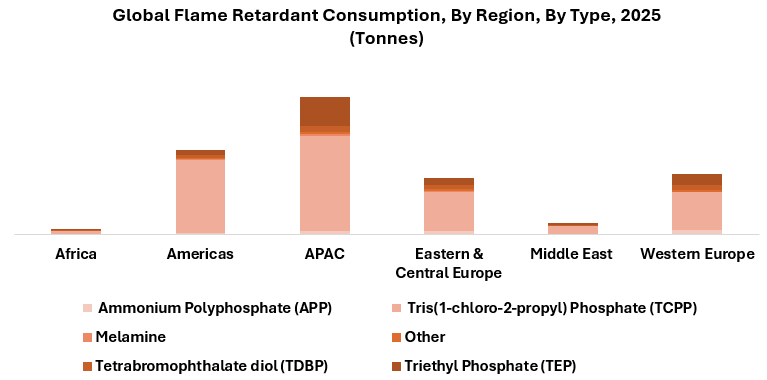

In 2025, global flame retardant (FR) consumption in polyurethane foams was largely shaped by evolving regulatory pressures and shifting chemical safety standards. Asia-Pacific (APAC) remained the largest regional market at nearly 40%, supported by its extensive polyurethane production base and continued use of cost‑effective halogenated FRs such as TCPP. However, as countries strengthen chemical management frameworks and adopt elements of EU REACH, RoHS and other global standards, demand for safer, non-halogenated alternatives is steadily rising across China, India and Southeast Asia.

The Americas accounted for around 24% of global FR demand, with the United States driving regional trends through stringent oversight under TSCA, EPA risk evaluations and California Proposition 65. These regulations have accelerated the transition away from certain halogenated FRs, particularly in flexible foam applications, although traditional chemistries still maintain a significant share due to performance requirements in furniture, bedding and automotive uses.

Europe, the Middle East and Africa (EMEA) collectively represented about 37% of global consumption, with Western Europe acting as the industry’s regulatory benchmark. Strict frameworks such as REACH, fire safety standards and circular economy policies have sharply reduced halogenated FR usage, boosting adoption of halogen‑free alternatives such as TEP, APP and melamine-based systems. Eastern and Central Europe are progressively aligning with EU chemical and fire safety legislation, resulting in a steady and more gradual shift toward environmentally preferred FRs.

The Middle East and Africa remain smaller and more price‑sensitive markets, where less stringent regulations allow continued reliance on traditional halogenated solutions. However, growing pressure from international trade requirements and multinational manufacturers is expected to drive longer‑term alignment with global trend.

By Type

The global flame retardant (FR) market for polyurethane foams in 2025 continued to be heavily dominated by TCPP (tris(1‑chloro‑2‑propyl) phosphate), which accounted for approximately 72% of total FR consumption. Its widespread use in both rigid and flexible foam applications, particularly in construction insulation, furniture, bedding and automotive seating, reflects its strong cost-to-performance balance. However, TCPP’s dominance is projected to decline as regulatory pressures on halogenated FRs intensify, supported by increasing scrutiny of toxicity, bioaccumulation and environmental persistence. These trends are prompting manufacturers to adopt safer, more sustainable alternatives across key markets.

Triethyl phosphate (TEP), currently representing around 16% of global consumption, is expanding rapidly as a leading non‑halogenated substitute. Its compatibility with flexible foams and alignment with Europe’s stringent chemical safety frameworks make it one of the most significant beneficiaries of the shift away from chlorine‑based chemistry.

Ammonium polyphosphate (APP) holds an estimated 4% share and is gaining traction as a high‑performance, halogen‑free additive in rigid foam systems, particularly in regions such as Western Europe where circular‑economy principles and REACH‑driven restrictions favour eco‑friendly phosphorus‑based FRs.

Expandable graphite (EG) is also emerging as a compelling non‑halogenated solution due to its excellent fire barrier performance and sustainability profile. Although still a smaller part of the market, EG’s growth trajectory is strong, especially in applications where enhanced fire resistance is required without compromising environmental credentials.

Tetrabromophthalate diol (TDBP) maintains a niche 5% market share, primarily in applications where stringent flame performance is essential and halogenated solutions are still permitted. Meanwhile, melamine and other specialty FRs, each representing less than 1%, serve targeted high‑performance markets such as automotive, electronics and specialty insulation systems.

By Application

Flame retardant use in polyurethane foams is strongly shaped by end‑use requirements, with domestic refrigeration standing as the largest application segment at nearly 20% of total demand, driven by strict fire safety standards and the extensive use of rigid PU foams in appliance insulation. Flexible‑faced and rigid‑faced insulation panels collectively account for about 25% of consumption, reflecting their central role in construction and building envelope systems. Spray-applied rigid foam also represents a significant share, while automotive seating foams follow closely, highlighting the sector’s ongoing reliance on flame-retarded polyurethane materials to meet stringent vehicle safety regulations.

The report is available at a price of €5,000. Please contact us for further information.

For more details, please contact: IAL Consultants

Email: ial@brggroup.com Or visit our website: www.ialconsultants.com